HP, one of the world’s biggest PC makers, may be preparing a significant shift in its component sourcing strategy as global DRAM shortages continue to tighten. With traditional memory suppliers struggling to meet demand, a new report indicates HP is exploring Chinese memory makers to help stabilize supply and keep products moving into key markets.

The core issue is simple: memory supply constraints are getting worse, not better. DRAM is a foundational component for laptops, desktops, and workstations, and when availability tightens, even major OEMs can end up competing for limited allocation. According to a recent Bank of America report shared by analyst commentary, HP has been discussing the qualification of additional memory suppliers from China, with the goal of supporting “limited” product shipments—particularly into Asia and Europe.

This matters because unlike specialized AI accelerators or proprietary compute hardware, memory chips are generally commodity components. That means OEMs can often swap suppliers more easily than they can with many other critical parts, as long as performance, reliability, and validation requirements are met. When supply from established giants becomes constrained, alternate suppliers quickly become more attractive—especially if they can deliver consistent volume at competitive pricing.

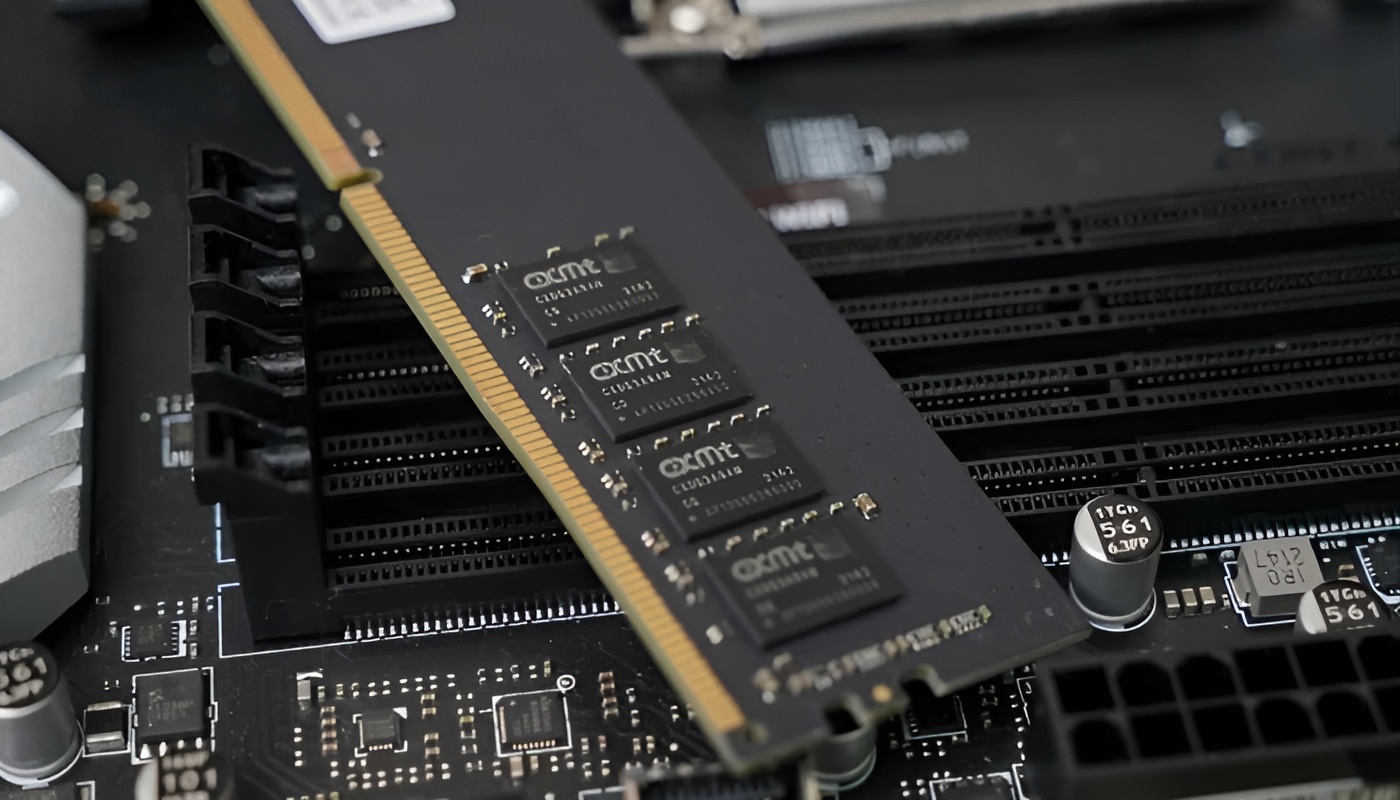

A major name in the conversation is CXMT, a Chinese DRAM producer that could become a meaningful option for consumer-focused products. CXMT’s DRAM wafer output is projected to reach as much as 300,000 units per month by 2026. While that figure is still below the scale of leading global memory manufacturers, it may be enough to ease pressure in select product segments, especially where supply is tightest.

CXMT is also thought to have sufficient capacity for DDR5 modules, in part because it has not yet seen widespread, aggressive adoption of its HBM efforts. With so much industry capacity being pulled toward high-bandwidth memory for AI systems, suppliers that are less exposed to HBM allocation pressures may have more room to support mainstream PC memory needs.

Adding to the momentum, CXMT is reportedly considering an IPO in Shanghai aimed at raising around $4.2 billion. If that funding push materializes, it would likely be directed toward expanding production capacity and accelerating research and development—two steps that could help the company compete more directly in the broader DRAM market over time.

Still, HP’s path isn’t straightforward. One of the biggest obstacles to using CXMT memory at scale is the regulatory environment in the United States. Under NDAA Section 5949, the U.S. Department of Defense is prohibited from sourcing semiconductors from CXMT, reflecting broader sensitivity about Chinese components in certain categories of technology. While commercial devices are not currently barred from using CXMT memory, the situation could evolve if adoption expands or policymakers introduce additional controls.

For now, the report suggests HP’s potential use of CXMT modules could be restricted to specific SKUs shipped outside the U.S., mainly in Asia and Europe. That approach could let HP reduce near-term supply risk without triggering the same level of regulatory exposure tied to U.S. government-related procurement rules.

The bigger takeaway is that Chinese memory and flash makers are increasingly positioned as a pressure-release valve for the PC industry. With AI-driven demand continuing to reshape how major suppliers allocate their output—often prioritizing data center and AI-related products—consumer markets may face ongoing constraints. Suppliers that are not heavily committed to HBM production could provide a temporary lifeline, helping OEMs maintain shipments while the market rebalances.