The Play Pendulum: Unraveling the Cyclical Nature of the Video Game Industry

Every week, business professor and author Joost van Dreunen delves into the fascinating intersections of gaming, tech, and entertainment in his SuperJoost Playlist. Recently, he has developed an intriguing thesis to explain the current volatility sweeping through the video game industry. While analysts and investors offer various explanations for the downturn in interactive entertainment, Joost suggests a deeper, cyclical pattern is at play.

Games aren’t created in isolation. The traditional belief suggests that technological advancement solely drives the evolution of games. Improved and faster hardware components have been viewed as the ultimate enablers of sophisticated gameplay because that’s what the market demands. Joost, however, proposes a different perspective: innovation cycles play a more significant role in shaping the industry’s direction than sheer technological advancements.

Often, what becomes popular in gaming is a direct result of technological limitations. Take Mario, for example; his iconic gloves and mustache were designed because the limited pixels could only do so much. By utilizing creative approaches to work around technical constraints, historically, games have achieved great success. The Nintendo Wii, for example, wasn’t the most powerful console of its time, but it succeeded spectacularly. Conversely, Google Stadia, despite its early advantage in cloud gaming, struggled to capture the market.

Throughout his recent discussions with industry leaders, Joost has discovered a partial explanation for the paradox of a highly successful yet tumultuous video game industry. Even the biggest players are currently rethinking their strategies. This insight has led to the formulation of what Joost calls the Play Pendulum theory.

The Play Pendulum theory suggests that the gaming industry swings between two primary types of innovation: content innovation and distribution innovation. Each cycle typically spans about a decade, impacting how games are created, distributed, and consumed. Understanding this cyclical pattern sheds light on the industry’s historical, current, and future trends.

Let’s break down these two types of innovation:

Content innovation focuses on developing new game types, expanding game portfolios, and pushing the boundaries of gameplay mechanics and storytelling. During these times, there’s strong and self-sustaining demand, prompting increased investment in content development.

Distribution innovation, on the other hand, is about finding novel ways to deliver games to players and generate revenue. This involves new platforms, innovative distribution methods, or unique monetization models. In these phases, industry growth is less certain, and companies focus on efficiency and market expansion.

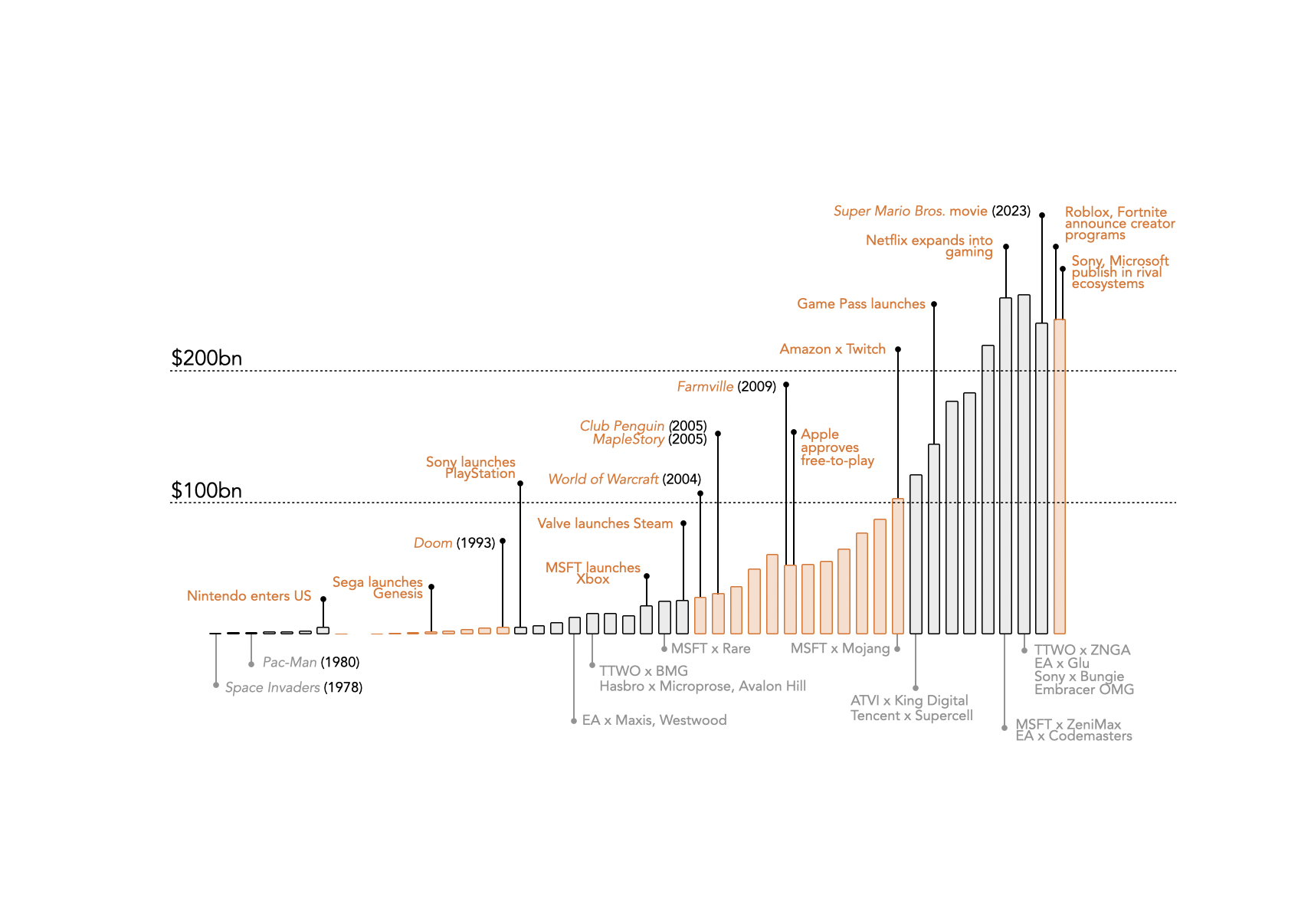

The early years of the gaming industry provide a vivid example of these innovation cycles. The first content innovation phase, from 1975 to 1983, saw Atari leading the charge with groundbreaking games like Pong and Space Invaders. Atari’s strategy of producing diverse game titles was initially successful, growing console sales from 250,000 units in 1977 to 4 million units annually by 1981 and 1982. However, an overemphasis on content led to market saturation and significant challenges, culminating in the industry crash of 1983.

Following the crash, the industry swung towards distribution innovation from 1984 to 1993. Nintendo emerged as a new leader, emphasizing quality control and a curated ecosystem. Their strict licensing for third-party developers and innovative retail terms helped rebuild consumer trust and revive the market. Between 1985 and 1993, the market grew from $429 million to $5.8 billion, thanks to Nintendo’s focus on distribution innovation.

The second major swing of the Pendulum saw the rise of 3D gaming, online multiplayer, and mobile gaming revolutions. From 1994 to 2003, content innovation was at its peak. Sony’s PlayStation set new standards for quality and performance, ushering in revolutionary games like Super Mario 64 and Tomb Raider. The market tripled from $5.8 billion in 1994 to $24.5 billion by 2003, driven by big publishers like Electronic Arts, who heavily invested in new intellectual properties.

Yet, this content-heavy approach brought new challenges, primarily rising development costs which averaged $10 million for new top-tier games. Prices for games didn’t keep pace with these costs, indicating an oversupply in the market.

The pendulum swung back towards distribution innovation from 2004 to 2015. This era saw the rise of social and mobile gaming, and the advent of digital distribution platforms. Valve’s Steam changed the game with a 70/30 revenue split and eliminated the need for expensive console certification or physical retail processes. Subscription-based models made a significant impact, with World of Warcraft peaking at 12.1 million subscribers in 2010.

Steam’s success led to a boom in game releases, growing from 1,500 titles annually to almost 15,000 new titles each year. World of Warcraft’s subscription model also proved groundbreaking, transforming how revenue could be generated in Western markets.

In essence, the Play Pendulum offers a fascinating lens through which we can understand the volatile yet highly productive nature of the video game industry. By recognizing the cyclical patterns of content and distribution innovation, we gain valuable insights into the industry’s past, present, and promising future.A new wave of game companies surged to prominence during this dynamic period in the gaming industry. Leading the charge was Nexon, which adeptly navigated the US market with blockbuster titles like MapleStory. Despite hurdles related to broadband penetration and payment methods, Nexon’s innovative distribution and payment strategies propelled its revenues from a modest $650,000 in 2005 to an impressive $29 million by 2007.

The game-changer, however, was mobile gaming. After the debut of the iPhone, Apple initially hesitated but eventually embraced free-to-play monetization. This shift significantly lowered entry barriers, allowing several newcomers to dominate the industry. Consequently, from 1994 to 2015, consumer spending on interactive entertainment skyrocketed from $5.8 billion to an astounding $104 billion.

A pivotal moment came in 2016 when Activision Blizzard acquired King Digital Entertainment, marking the industry’s intensified focus on mobile and casual gaming. This era saw the explosive rise of battle royale games, live service models, and increased emphasis on user-generated content. Epic Games, for example, transformed its fortunes by reimagining Fortnite with battle royale gameplay, establishing itself as a top publisher.

As online play became the norm, gamers spent more time playing and socializing virtually. Cross-platform play interconnected gamers worldwide. In this context, Microsoft’s strategic acquisitions of Mojang (Minecraft) in 2014, Bethesda in 2021, and Activision Blizzard in 2023 were particularly notable.

The COVID-19 pandemic further accelerated demand, fueling numerous acquisitions across the industry. By 2023, the ten largest game companies controlled 65 percent of the global games market, up from 58 percent in 2020. Their combined revenue surged from $45.4 billion in 2014 to an impressive $157.9 billion by 2023, more than tripling.

However, this rapid growth was not without risks. Take-Two Interactive’s $12.7 billion acquisition of Zynga in 2022 led to an immediate decline in the company’s value. Similarly, Microsoft’s $68.7 billion acquisition of Activision Blizzard coincided with Candy Crush losing its top spot, underscoring the challenges of maintaining dominance in the fast-evolving mobile market.

In 2024, the focus is swinging back toward distribution innovation. The release of the Super Mario Bros. Movie and new creator tools for popular games are creating new distribution channels and revenue models. Hollywood is capitalizing on gaming IPs for film productions, expanding the audience and opportunities for game companies.

The launch of the Unreal Editor for Fortnite (UEFN) and the Roblox Economy exemplify a paradigm shift. Both Epic Games and Roblox are now placing user-generated content at the core of their strategies. Echoing this trend, Electronic Arts announced a creator program for The Sims as part of its growth strategy.

Market structure has shifted in tandem with these strategic innovations. During periods of content innovation, we see market consolidation, as firms pursue economies of scale. However, distribution innovation phases often reduce market concentration as new entrants exploit novel methods.

Historical data reveals this. In the early 1980s, Atari’s dominance ultimately led to an industry crash due to overextension. The market revitalized with Nintendo, and competitors like Sega and Sony joined the fray, initially decreasing market concentration. The launch of Steam in 2003 and the advent of social network-based and mobile gaming further dispersed market concentration.

However, as the latest content innovation phase peaked, large game companies returned to capturing market share through acquisitions, increasing market concentration. This oscillating focus between content and distribution innovation often aligns with financial downturns. For example, before the video game crash in 1983, an economic downturn struck the US. Similarly, before smartphones rose in 2008 and once more in 2023, economic slowdowns paralleled these market shifts.

The Play Pendulum theory helps explain the cyclical nature of innovation in the video game industry, suggesting that companies recognizing these shifts are well-positioned for success. Yet, it’s important to acknowledge this model’s limitations as it simplifies complex industry dynamics. While it effectively tracks broad trends, predicting specific innovations remains challenging due to the industry’s rapid evolution.

As we stand at the brink of a new era shaped by distribution innovation, the possibilities are vast. Emerging platforms may redefine our gaming experiences, and new monetization models could reshape creator-consumer dynamics. The real question is which companies will seize this moment to steer the industry’s future.