Samsung Advisor Predicts Memory Chip Prices Could Drop in Late 2027 as China Expands DRAM Production

Memory chip prices have surged sharply as artificial intelligence demand continues to reshape the semiconductor industry, but one former Samsung Electronics executive believes relief may be on the way. Kye-hyun Kyung, an advisor to Samsung Electronics and former head of the company’s Device Solutions division, expects memory prices to begin falling in the second half of next year if China’s aggressive production expansion delivers a major supply increase.

The global memory market has been under intense pressure due to the rapid growth of AI computing. High-bandwidth memory, or HBM, has become one of the most important components for advanced AI accelerators, and demand has outpaced supply across the industry. As manufacturers shift more capacity toward HBM, shortages have also affected other memory categories, including DDR5 DRAM.

This supply imbalance has pushed prices higher across multiple markets. DDR5 memory, in particular, has seen steep increases as PC makers, server companies, and technology firms compete for available inventory. In some regions, DDR5 pricing has reportedly climbed several hundred percent compared with previous levels, forcing companies to place orders earlier than usual to avoid even higher costs later.

The impact has reached the personal computer market as well. Major hardware companies have seen shipment patterns shift as customers and businesses move to purchase systems before memory price hikes fully filter through to retail products. Since memory is a key cost component in laptops, desktops, servers, and workstations, rising DRAM prices can quickly affect the broader electronics supply chain.

Kyung said that China’s memory chip industry could play a major role in changing the current market direction. Speaking at the 285th National Academy of Engineering of Korea Forum, he noted that Chinese semiconductor companies are investing heavily to expand memory production capacity. If those investments succeed and lead to higher output, the market could face a supply surge that brings prices down in the second half of 2027.

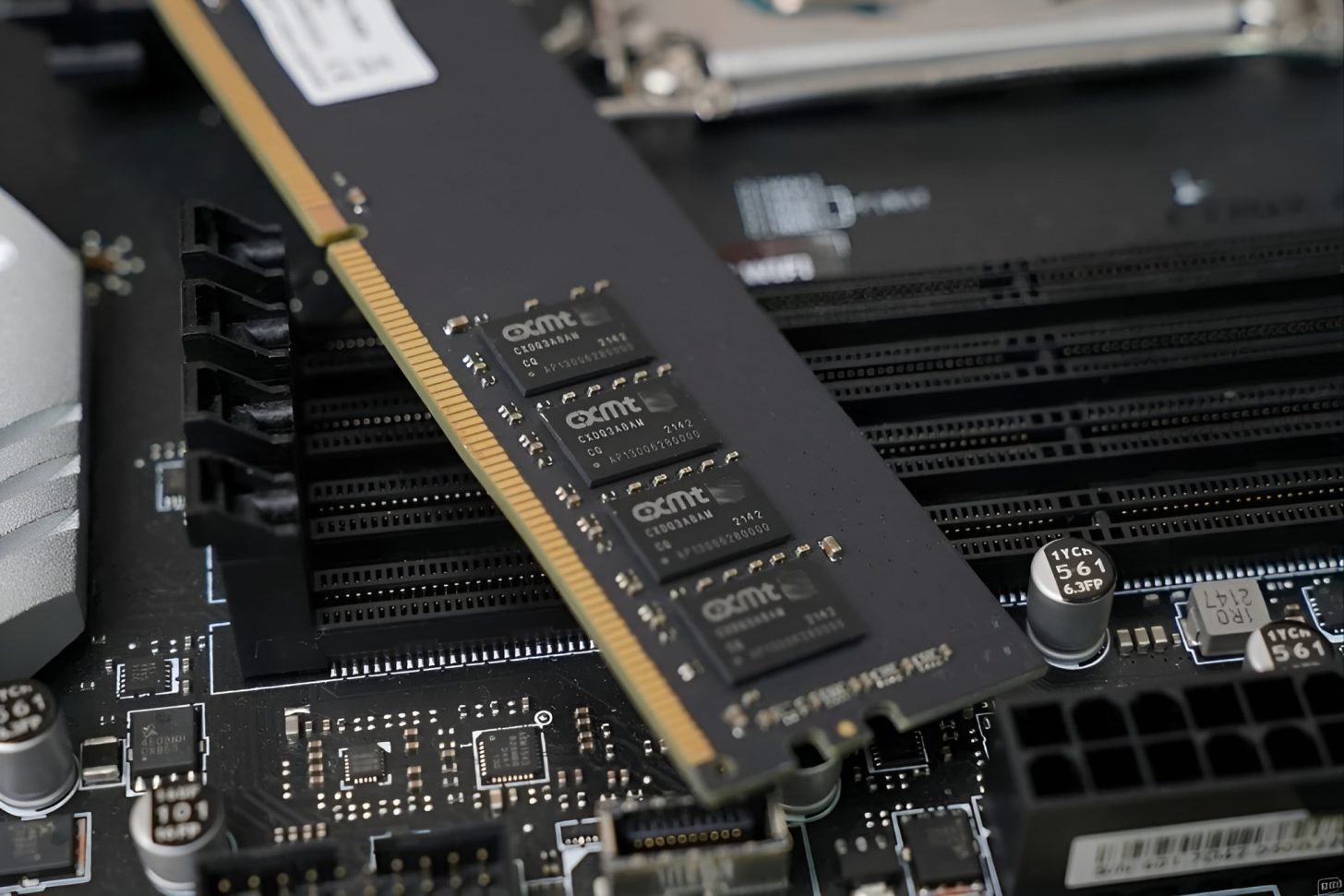

Chinese DRAM manufacturers have been working to strengthen their position in the global memory market, with ChangXin Memory Technologies widely seen as one of the country’s most important players. The company has been increasing its focus on DDR5, a memory standard that is essential for modern PCs, servers, and data center systems. Other Chinese firms are also trying to gain ground as demand for advanced memory continues to rise.

Kyung pointed to market research estimates suggesting that memory production capacity could reach around six million wafers per month in the second half of 2027. Such a large increase would represent a major shift in supply, especially if it arrives while demand growth begins to normalize.

However, he also warned that the outlook is not guaranteed. The pace of memory investment depends heavily on the spending plans of major technology companies. If large AI infrastructure buyers begin to see weaker returns from their capital expenditure, memory manufacturers may slow expansion plans. A pullback in AI-related spending could reduce the incentive to build new capacity, delaying or limiting any expected supply increase.

The comments highlight the delicate balance currently shaping the semiconductor market. AI demand has created a powerful growth cycle for HBM and advanced memory, benefiting major chipmakers but also creating cost pressure for downstream industries. At the same time, a wave of new production capacity, particularly from China, could eventually reverse the shortage and push prices lower.

Kyung also emphasized that South Korea must strengthen its role beyond memory manufacturing. He argued that Korea needs to expand its presence in the global fabless semiconductor market to stay competitive against the United States and China. While Korean companies are global leaders in memory chips, the fabless sector, where firms design chips but outsource production, remains an area where the country has room to grow.

His remarks reflect a broader concern in the semiconductor industry: memory leadership alone may not be enough as competition intensifies across AI processors, chip design, advanced packaging, and foundry services. As the US and China push deeper into strategic chip development, South Korea may need to diversify its semiconductor strengths to protect its long-term position.

For consumers and businesses, the key takeaway is that memory prices may remain elevated in the near term, especially as AI servers continue to absorb high-end components. But if China’s production expansion reaches scale by late 2027, the market could shift from shortage to oversupply, bringing lower prices for DDR5, server memory, and potentially other DRAM products.

The next year will be critical for the memory chip market. AI demand, Chinese DRAM output, global technology spending, and fabless chip competition will all influence whether prices remain high or begin to fall. For now, Kyung’s forecast offers a possible timeline for relief: the second half of 2027, when new supply may finally catch up with the AI-driven memory boom.

— The First RAM Module With an OLED Screen")